Fed Chair Nominee Kevin Warsh Aims to Transform the Central Bank — and the Biggest Loser May Be Wall Street – The Motley Fool

History is about to be made at America’s premier financial institution, the Federal Reserve.

May 15 will mark Jerome Powell’s final day as Fed chair and might represent the start of Kevin Warsh’s tenure as head of the Fed (pending Senate confirmation). It may also mark a turning point for the iconic Dow Jones Industrial Average (^DJI 0.31%), broad-based S&P 500 (^GSPC +0.29%), and growth-driven Nasdaq Composite (^IXIC +0.89%).

Jerome Powell’s term as Fed chair wraps up on May 15. Image source: Official Federal Reserve Photo.

Jerome Powell’s tenure as Fed chair ends in less than two weeks

President Donald Trump and Powell have been publicly clashing over interest rates since the president’s second, non-consecutive term began in January 2025. Trump has opined that the Federal Open Market Committee (FOMC) should aggressively cut interest rates to 1% or lower, while Powell has contended that the FOMC will base its monetary policy decisions on economic data, not political persuasion. The FOMC is the 12-person body, including the Fed chair, that sets the nation’s monetary policy.

With the writing on the wall for the last year that Powell wouldn’t be back, Trump nominated Kevin Warsh on Jan. 30 to become the 17th Federal Reserve chair.

On the surface, Warsh is a logical selection. He previously served on the Board of Governors of the Federal Reserve and was a voting member of the FOMC from Feb. 24, 2006, to March 31, 2011. This means he played an instrumental role in steering the U.S. economy through the financial crisis.

But just because Kevin Warsh would bring experience to the position, this doesn’t mean Wall Street will benefit.

Image source: Getty Images.

Kevin Warsh lays out his plan to transform the Fed

The stock market thrives on continuity and predictability. Regardless of whether Jerome Powell and the FOMC made the right or wrong policy decisions, investors almost always knew what to expect. Powell’s views on inflation, unemployment, and economic growth have been steady throughout his tenure.

If Kevin Warsh is confirmed as the next Fed chair, potentially all of this changes.

On April 21, Warsh testified in front of the Senate Banking Committee for 2.5 hours. While some senators grilled the prospective next head of the Fed about central bank independence in light of Trump’s comments calling for lower interest rates, it was his commentary about the future of America’s foremost bank that turned heads.

For example, Warsh wants to completely overhaul the central bank’s approach to inflation. Instead of aiming for a long-standing inflation target of 2%, Warsh told the Senate Banking Committee, “I believe that price stability should be a change in prices such that no one’s talking about it.” This relatively vague definition would leave the door open for interest rates to remain higher over a longer period, and for price stability to become the more important aspect of the dual mandate (price stability and maximize employment).

“If Trump wants someone easy on inflation, he got the wrong guy in Kevin Warsh.”@AnnaEconomist pic.twitter.com/FGMfeSqHpU

— Daily Chartbook (@dailychartbook) January 31, 2026

Rethinking the definition of inflation is noteworthy, given that Warsh was labeled a hawk for his FOMC voting record during the financial crisis. Even as the unemployment rate soared, Warsh regularly cautioned of inflationary pressures if interest rates were lowered.

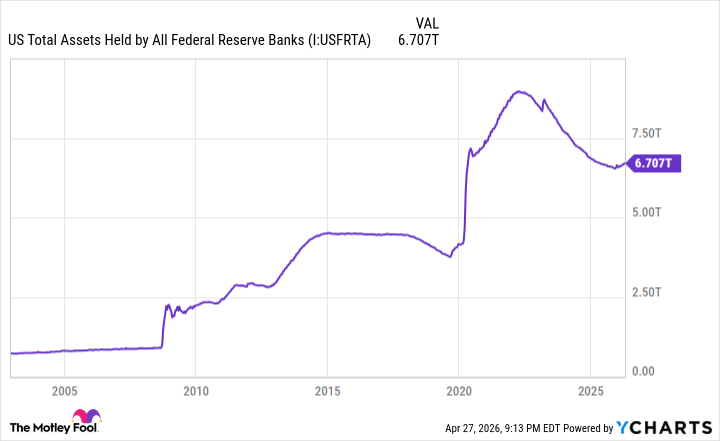

Kevin Warsh also wants to transform the central bank’s balance sheet, which stands at approximately $6.7 trillion and is primarily comprised of long-term U.S. Treasury bonds and mortgage-backed securities. During his testimony, he partially lumped the blame for higher inflation on this bloated balance sheet.

The Fed chair nominee favors deleveraging this balance sheet, with the Fed transitioning into a passive role in markets.

A Warsh-led Fed could be nightmare fuel for the stock market

The issue for Wall Street isn’t whether deleveraging the Federal Reserve’s balance sheet and/or changing the definition of inflation is the right or wrong move. Rather, it’s how these actions can impact the Dow Jones Industrial Average, S&P 500, and Nasdaq Composite over the next few years.

According to the S&P 500’s Shiller Price-to-Earnings Ratio, the stock market entered 2026 at its second-priciest valuation over 155 years. While the rise of artificial intelligence and record S&P 500 share buybacks have helped support this valuation premium, the expectation of additional rate cuts by the FOMC was at or near the top of the list.

Between the inflationary effects of the Iran war and Kevin Warsh’s vision for the central bank under his leadership, the prospect of lower interest rates has been tossed out the window — and that’s nightmare fuel for an expensive stock market.

US Total Assets Held by All Federal Reserve Banks data by YCharts.

For instance, Warsh’s desire to shrink the Fed’s balance sheet can drive up lending costs, even if the FOMC doesn’t act by traditional means (e.g., raising the federal funds target rate). Since bond prices and yields are inversely related, selling trillions of dollars in U.S. Treasury bonds would be expected to drive up yields, thereby increasing borrowing costs.

Again, this isn’t a judgment of whether deleveraging the balance sheet is the right or wrong move. Rather, it’s to point out that Warsh’s proposed transformation would have potentially deleterious consequences for an already pricey stock market.

The same can be said for Warsh’s preferred definition of inflation. Removing a hard target of 2% for “a change in prices such that no one’s talking about it” leaves the door open for FOMC rate hikes and extended periods of higher interest rates. It’s not a particularly inviting scenario for tech companies spending tens or hundreds of billions on artificial intelligence infrastructure.

A history-making moment for the Federal Reserve could mark the beginning of a period of heightened uncertainty and volatility for Wall Street.